PredSales

Ra’Shawn Howard

Libraries I Use

library(tidyverse)

library(forecast)## Registered S3 method overwritten by 'quantmod':

## method from

## as.zoo.data.frame zoo##

## Attaching package: 'forecast'## The following object is masked from 'package:yardstick':

##

## accuracylibrary(feasts)## Loading required package: fabletools##

## Attaching package: 'fabletools'## The following objects are masked from 'package:forecast':

##

## accuracy, forecast## The following object is masked from 'package:yardstick':

##

## accuracy## The following object is masked from 'package:parsnip':

##

## null_model## The following object is masked from 'package:infer':

##

## generatelibrary(fable)

library(tsibble)

library(lubridate)##

## Attaching package: 'lubridate'## The following object is masked from 'package:tsibble':

##

## interval## The following objects are masked from 'package:base':

##

## date, intersect, setdiff, unionlibrary(tidymodels)Load Data

sales_data <- read_csv("/Users/rashawnhoward/Downloads/sales_train.csv")##

## ── Column specification ────────────────────────────────────────────────────────

## cols(

## date = col_character(),

## date_block_num = col_double(),

## shop_id = col_double(),

## item_id = col_double(),

## item_price = col_double(),

## item_cnt_day = col_double()

## )glimpse(sales_data)## Rows: 2,935,849

## Columns: 6

## $ date <chr> "02.01.2013", "03.01.2013", "05.01.2013", "06.01.2013"…

## $ date_block_num <dbl> 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, …

## $ shop_id <dbl> 59, 25, 25, 25, 25, 25, 25, 25, 25, 25, 25, 25, 25, 25…

## $ item_id <dbl> 22154, 2552, 2552, 2554, 2555, 2564, 2565, 2572, 2572,…

## $ item_price <dbl> 999.00, 899.00, 899.00, 1709.05, 1099.00, 349.00, 549.…

## $ item_cnt_day <dbl> 1, 1, -1, 1, 1, 1, 1, 1, 1, 3, 2, 1, 1, 2, 1, 2, 1, 1,…Explore/Clean Data

The data being from kaggle it fairly clean, we just need to get the data into the correct format to perform our analysis. The Competetion wanted to predict total sales for each shop, while we will be predicting total sales as a whole. From the glimpse function we can see that the date column is of type chr and needs to be converted to type Date, also item cnt day will need to summed for the different shops on the same date (e.g we will group_by date). The chunck of code below will do this.

sales_data %>%

mutate(date = dmy(date)) %>% # Change date column to type date

group_by(date) %>%

summarise(item_cnt_day = sum(item_cnt_day)) %>%

as_tsibble(index = date) -> sales_data # Make data a time series object (easier to work with)!## `summarise()` has ungrouped output. You can override using the `.groups` argument. # Assign changes to sales datavisualize data

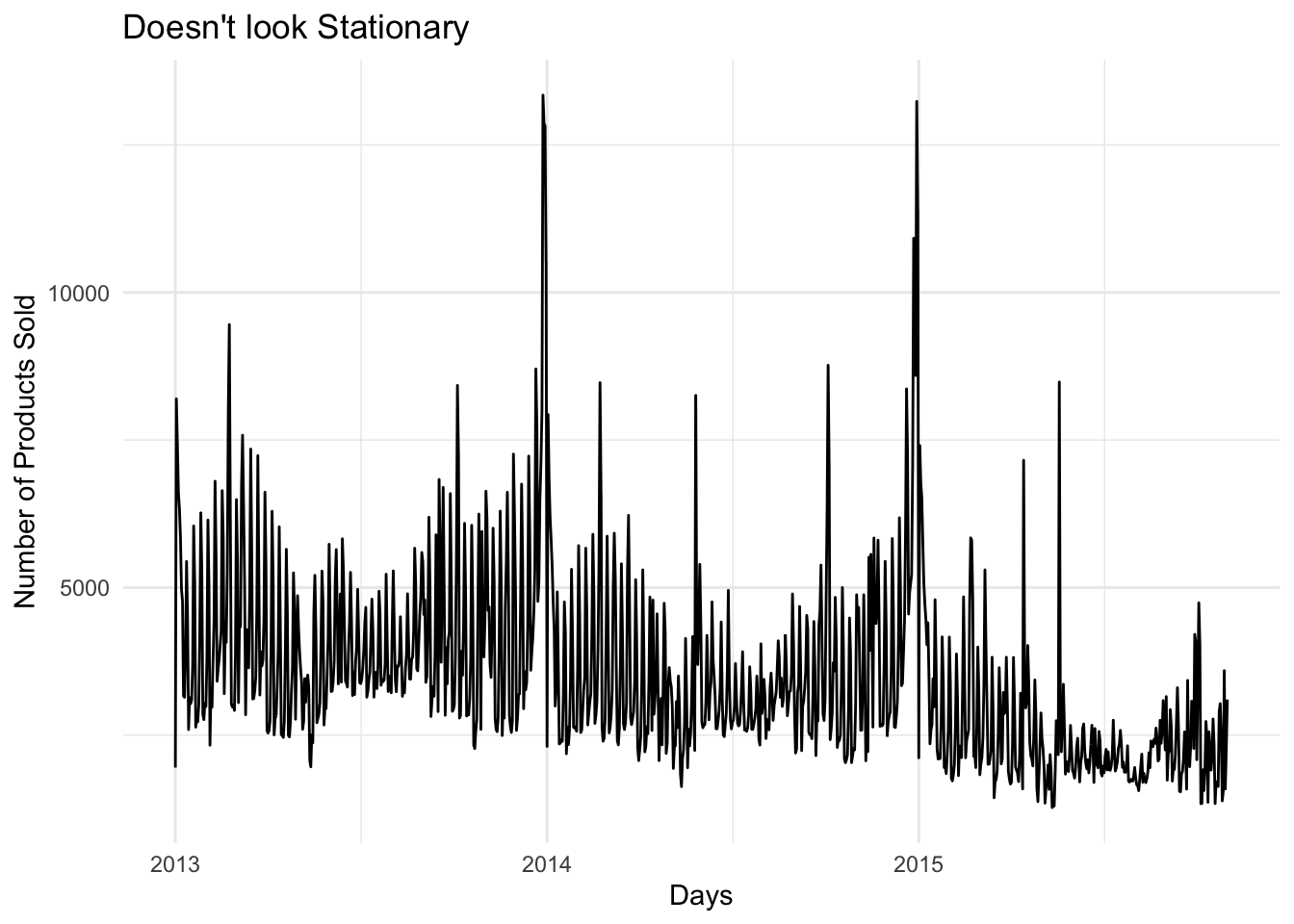

The data Doesn’t look stationary. We can see a slight trend downward in the recent year. Two higher than normal peeks at the beginning of 2014 and the begining of 2015, I’m not sure what caused these peeks, but this should be fixed with a tranformation. We can see a cyclic and seasonal pattern in the data as well and should be taken into account when modeling.

sales_data %>%

ggplot(aes(date,item_cnt_day)) +

geom_line() +

xlab("Days") +

ylab("Number of Products Sold") +

ggtitle("Doesn't look Stationary")

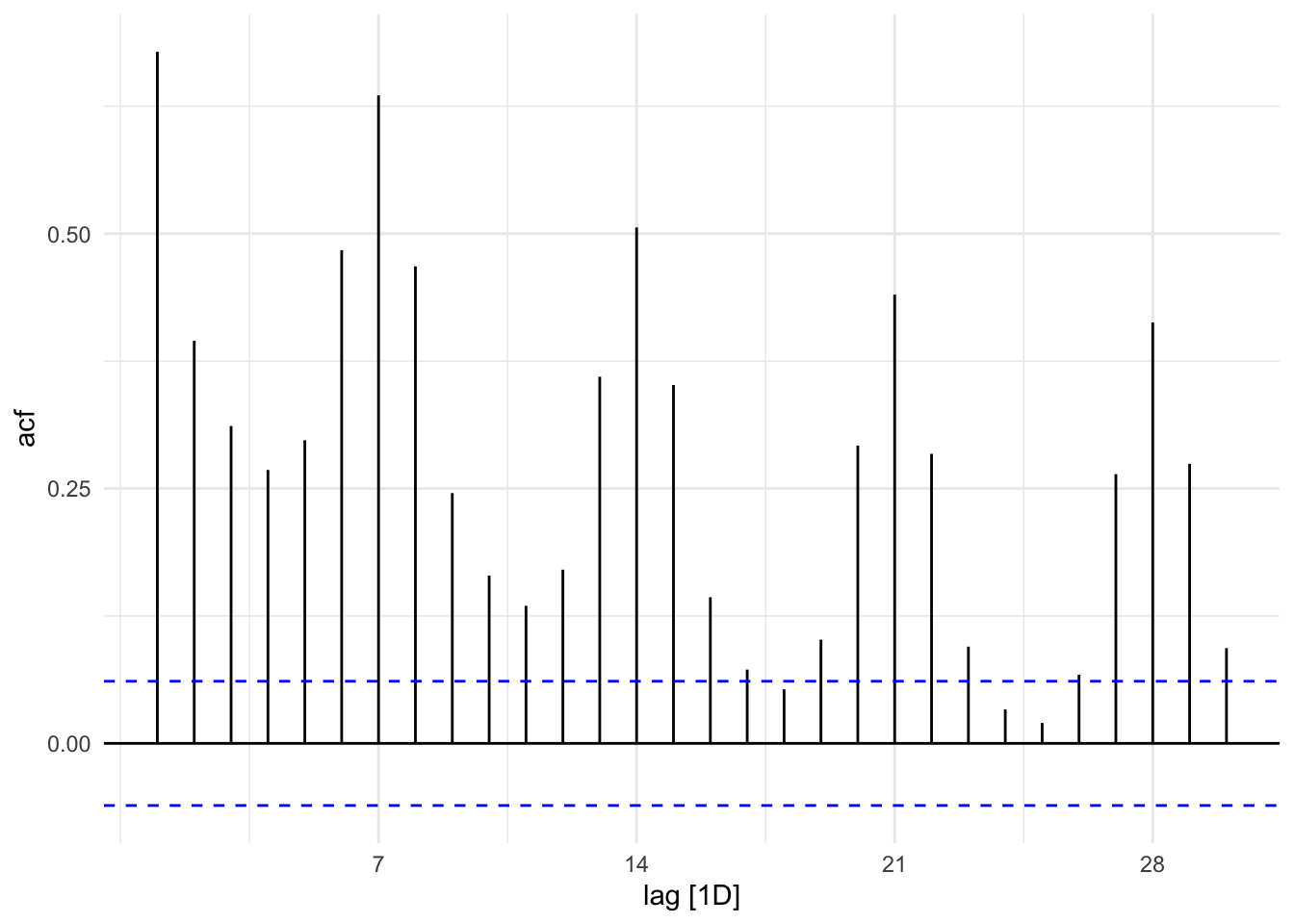

Looking at the ACF plot below we can see that the data has high peeks at 7, 14, 21, and 28. Suggesting that the data is weekly seasonal.

sales_data %>%

ACF() %>%

autoplot()## Response variable not specified, automatically selected `var = item_cnt_day`

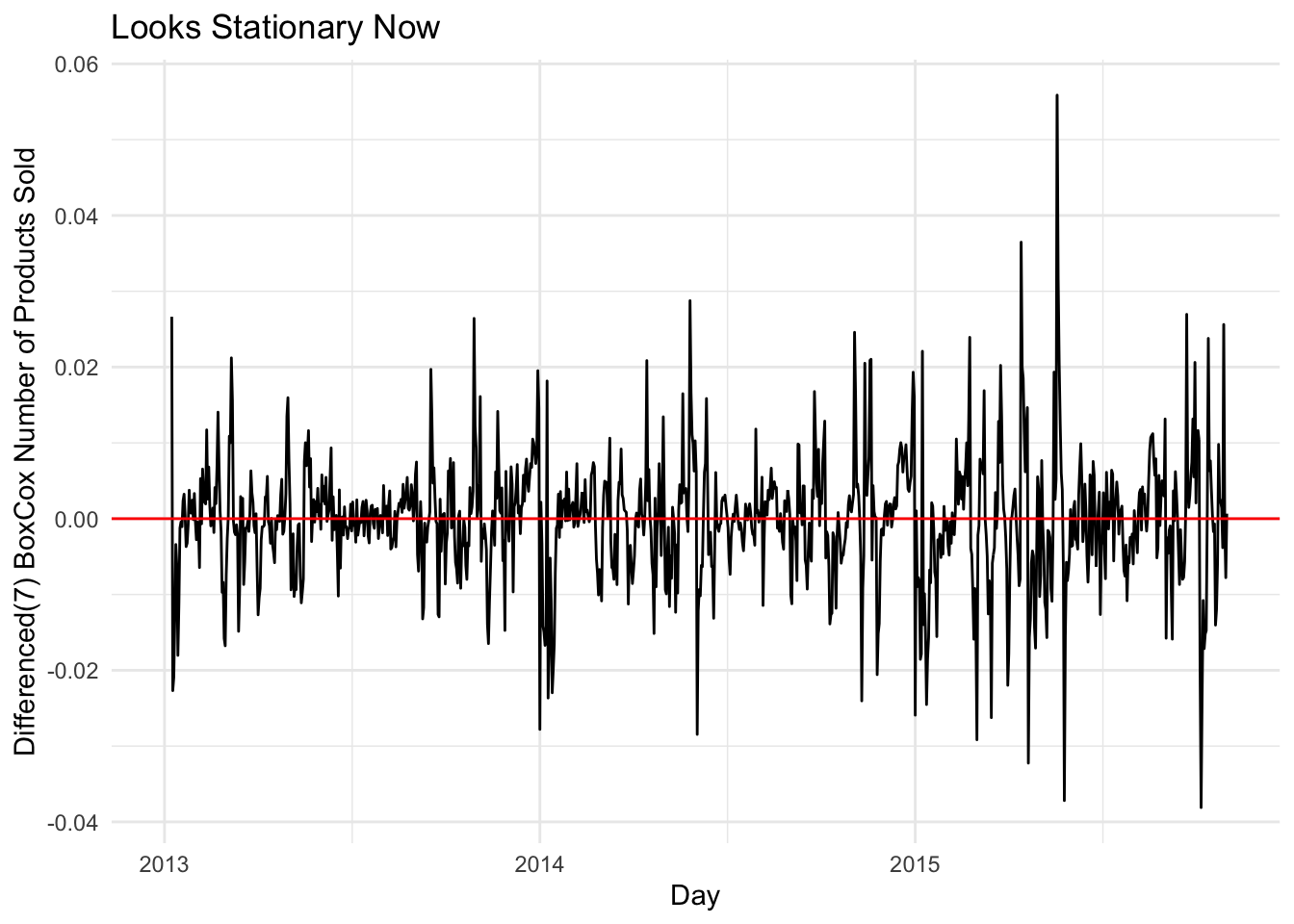

We can see the BoxCox fixed the Variance issue from the first plot, and we can see stationarity from second plot. We can also add another difference on to this, looking at the nsdiff and ndiff function we see that the data needs a seasonal difference and a regular difference.

lambda <- sales_data %>% # Find Best Lambda Value

features(item_cnt_day,features = guerrero) %>%

pull(lambda_guerrero)

sales_data %>% # Apply BoxCox Transformation # assign to sales data

mutate(item_cnt_day = box_cox(item_cnt_day,lambda)) -> sales_data

sales_data %>% # Plot what data looks like now

autoplot() +

xlab("Day") +

ylab("BoxCox Number of Products Sold") +

ggtitle("The Variance Issue Is Gone") # still see trend, need to diffference data## Plot variable not specified, automatically selected `.vars = item_cnt_day`

# What kind of differences do we need?

sales_data %>%

features(item_cnt_day,unitroot_ndiffs) # We have a trend component## # A tibble: 1 x 1

## ndiffs

## <int>

## 1 1sales_data %>%

features(item_cnt_day,unitroot_nsdiffs) # We have a seasonal component## # A tibble: 1 x 1

## nsdiffs

## <int>

## 1 1sales_data %>% # Plot to see if data is stationary

mutate(item_cnt_day = difference(item_cnt_day,7)) %>%

autoplot() +

geom_hline(yintercept = 0, col="red") +

xlab("Day") +

ylab("Differenced(7) BoxCox Number of Products Sold") +

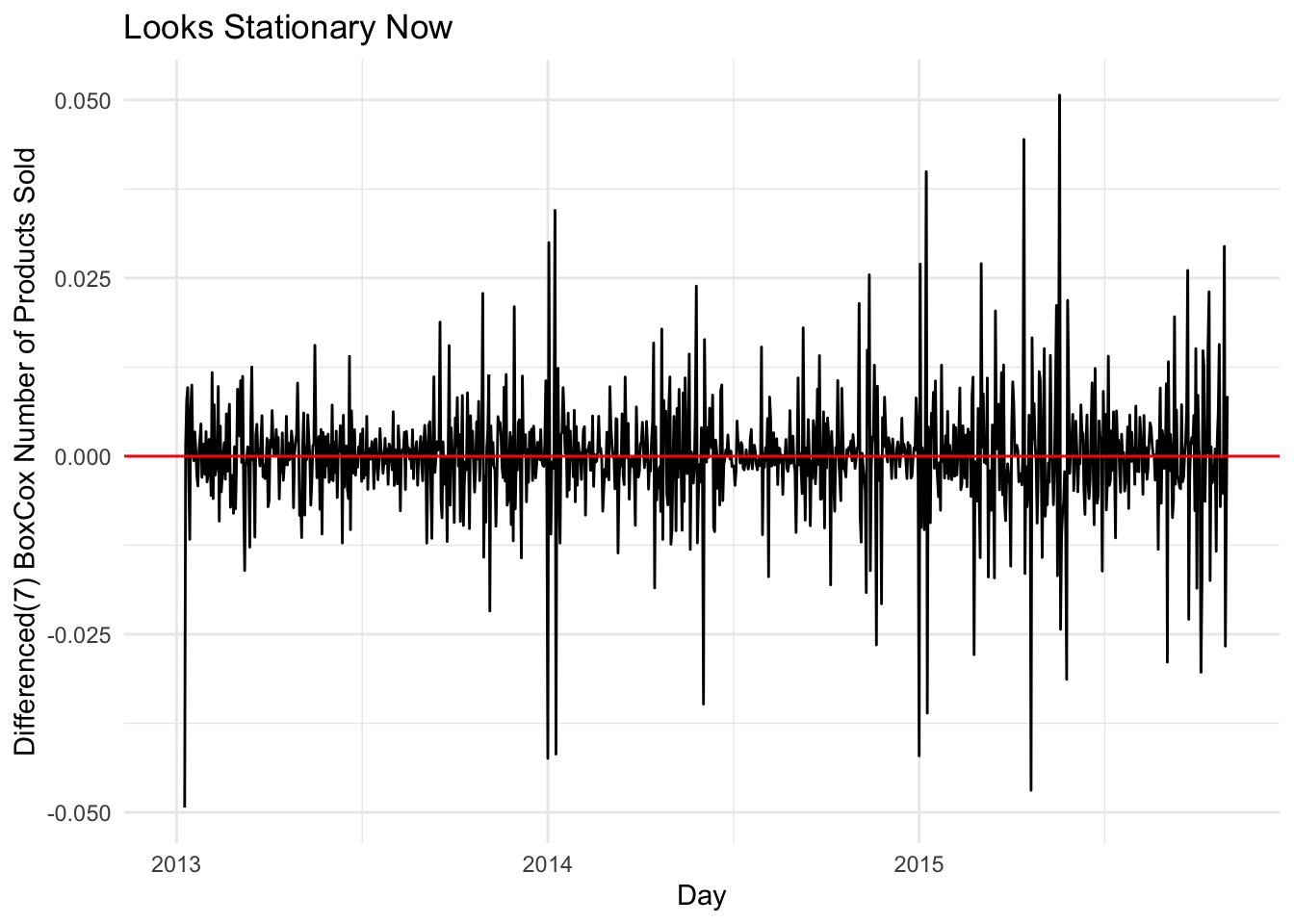

ggtitle("Looks Stationary Now")## Plot variable not specified, automatically selected `.vars = item_cnt_day`

sales_data %>% # Plot to see if data is stationary (extra difference plot)

mutate(item_cnt_day = difference(item_cnt_day,7) %>% difference()) %>%

autoplot() +

geom_hline(yintercept = 0, col="red") +

xlab("Day") +

ylab("Differenced(7) BoxCox Number of Products Sold") +

ggtitle("Looks Stationary Now")## Plot variable not specified, automatically selected `.vars = item_cnt_day`

Split Data

Make a training and test set

split <- initial_time_split(sales_data,prop = 0.8)

test <- testing(split)

train <- training(split)Modeling

Picking p and q for SARIMA model

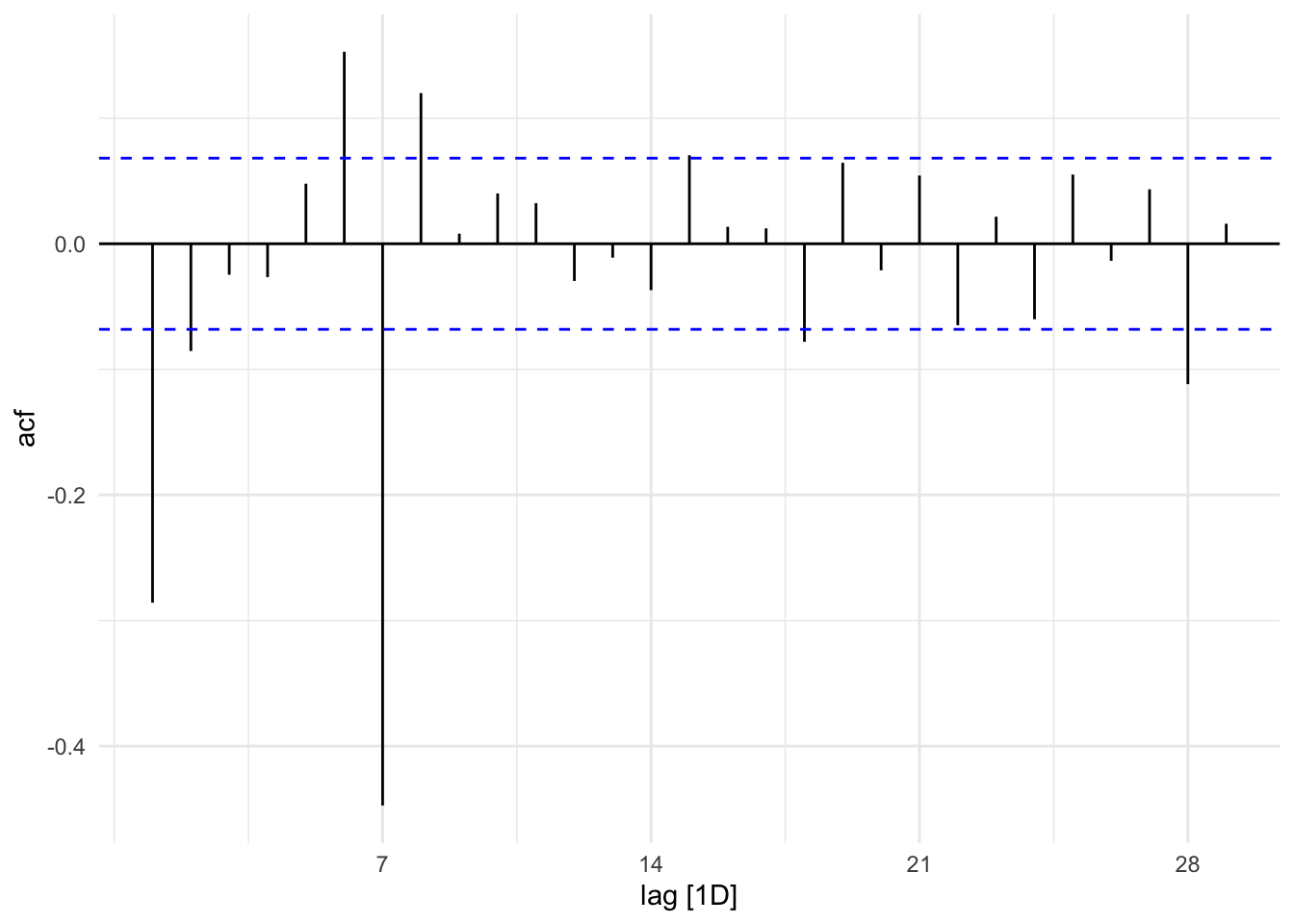

Looking at the ACF plot below, we see a big lag at 7 this suggest a seasonal MA component. There is also a lag at 28 This might suggest 2 seasonal MA components, but this lag is really small and we may not need this component(we can test different models). We can see some other regular MA components 2 maybe 4.

train %>%

mutate(item_cnt_day = difference(item_cnt_day,7) %>% difference()) %>%

ACF() %>%

autoplot()## Response variable not specified, automatically selected `var = item_cnt_day`

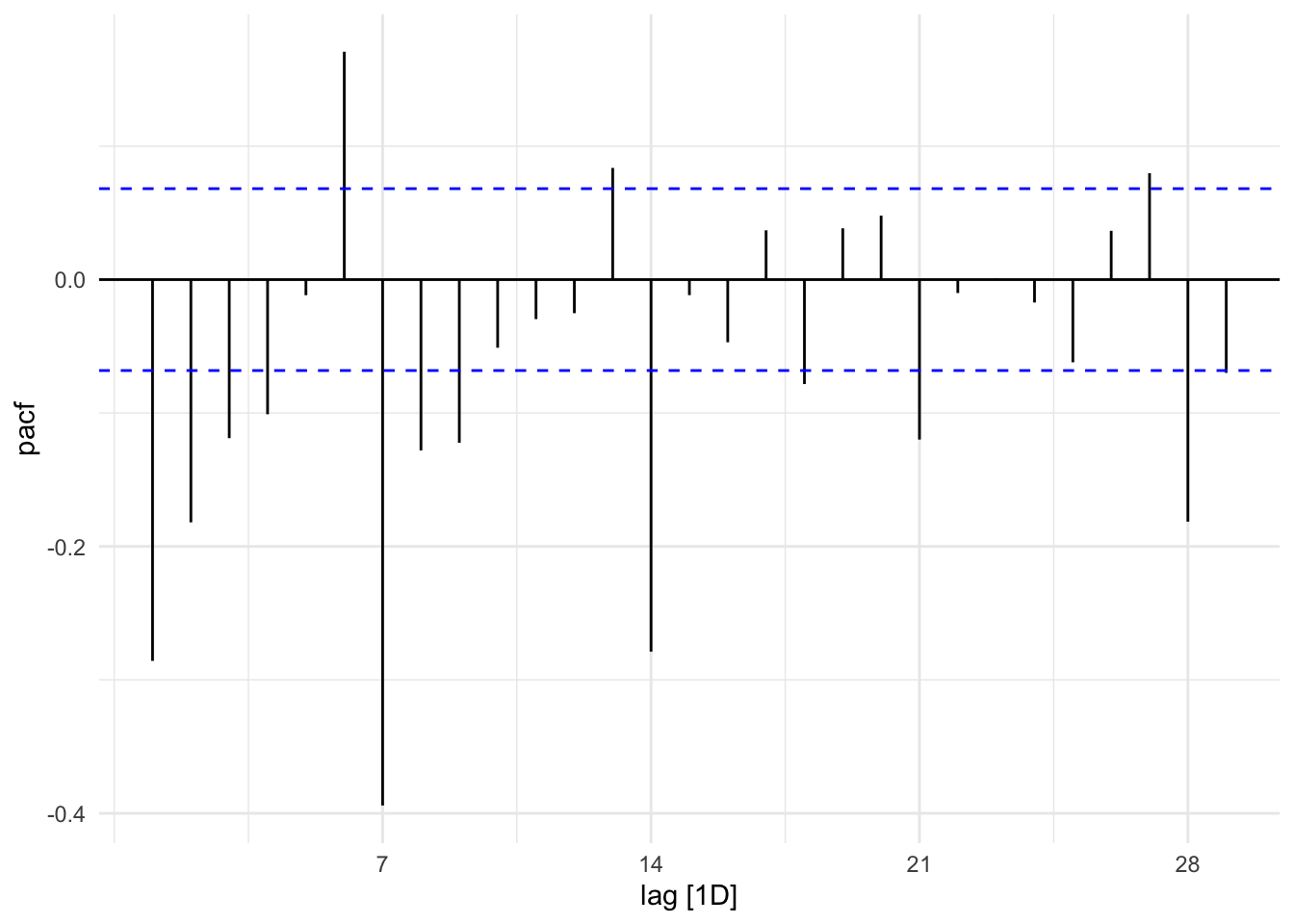

Looking at the PACF plot below, we can see big lags at 7, 14, 21, and 28 which could suggest 4 seasonal AR componets. Its hard to tell how many regular components could be 2 or more.

train %>%

mutate(item_cnt_day = difference(item_cnt_day,7) %>% difference()) %>%

PACF() %>%

autoplot()## Response variable not specified, automatically selected `var = item_cnt_day`

The EACF plot suggest an MA(2) ARMA(2,2) ARMA(3,1)

TSA::eacf(train$item_cnt_day)## Registered S3 methods overwritten by 'TSA':

## method from

## fitted.Arima forecast

## plot.Arima forecast## AR/MA

## 0 1 2 3 4 5 6 7 8 9 10 11 12 13

## 0 x x o o x x x x x o o o x x

## 1 x x x o o x x x x x o o x x

## 2 x x o o o o x x x o o o o x

## 3 x o x o o o x x o x o o o x

## 4 x x o o o o x x x o o o o x

## 5 x x x o o x x x x o o o x x

## 6 x x x o x x x x x o x x x x

## 7 x x x x x x x x o o o o o oDifferent models

Seems my model has a lower AICc score than the automated model

train %>% # Automated model chosen by auto.arima function

model(ARIMA(item_cnt_day,stepwise=FALSE,approximation = FALSE)) %>%

report()## Series: item_cnt_day

## Model: ARIMA(4,0,0)(0,1,1)[7]

##

## Coefficients:

## ar1 ar2 ar3 ar4 sma1

## 0.5921 0.0517 0.0358 0.0853 -0.9171

## s.e. 0.0371 0.0418 0.0421 0.0363 0.0325

##

## sigma^2 estimated as 2.648e-05: log likelihood=3154.27

## AIC=-6296.54 AICc=-6296.43 BIC=-6268.28train %>% # My model

model(ARIMA(item_cnt_day~pdq(p=2:4,0:2,q=2:4,p_init=2,q_init=2)+PDQ(P=1:4,1,Q=0:2,P_init=1,Q_init=1))) %>%

report()## Series: item_cnt_day

## Model: ARIMA(2,0,2)(2,1,0)[7]

##

## Coefficients:

## ar1 ar2 ma1 ma2 sar1 sar2

## 0.7758 0.0444 -0.2288 -0.1342 -0.6031 -0.2997

## s.e. 0.4516 0.3485 0.4492 0.1211 0.0362 0.0352

##

## sigma^2 estimated as 3.126e-05: log likelihood=3091.41

## AIC=-6168.82 AICc=-6168.68 BIC=-6135.86Fit

fit <- train %>%

model(arima_400_011 = ARIMA(item_cnt_day~pdq(4,0,0)+PDQ(0,1,1)),

arima_202_210 = ARIMA(item_cnt_day~pdq(2,0,2)+PDQ(2,1,0)),

arima_111_111 = ARIMA(item_cnt_day~pdq(1,1,1) + PDQ(1,1,1)),

lm1 = ARIMA(item_cnt_day~0+date+pdq(4,0,0)+PDQ(0,1,1)),

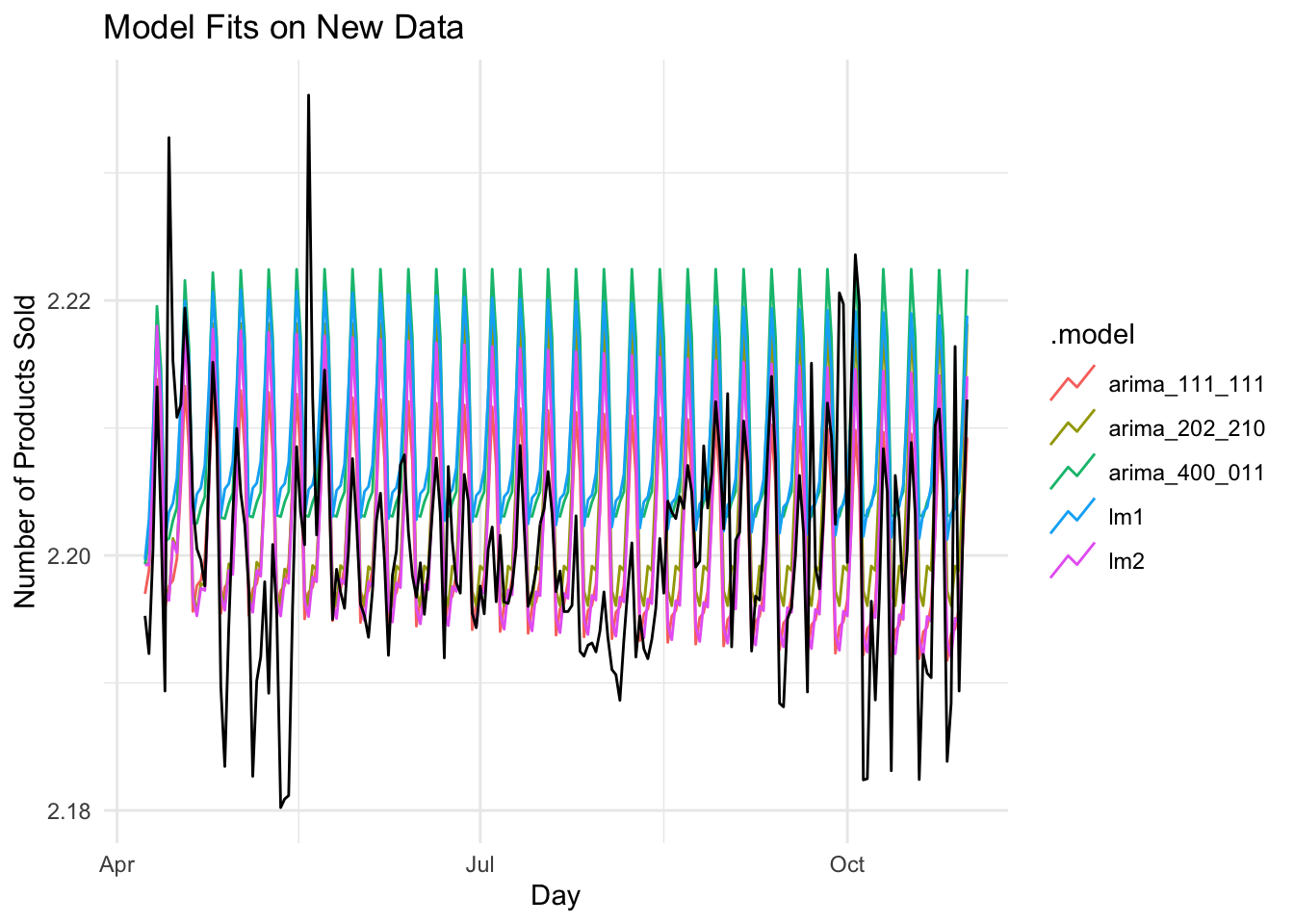

lm2 = ARIMA(item_cnt_day~0+date+pdq(2,0,2)+PDQ(2,1,0)))fit %>%

forecast(test) %>%

autoplot(test,level = NULL) +

xlab("Day") +

ylab("Number of Products Sold") +

ggtitle("Model Fits on New Data")

Looks like the arima_111_111 model did the best on the test set with RMSE = 0.008234140

fit %>%

forecast(test) %>%

fabletools::accuracy(test)## # A tibble: 5 x 9

## .model .type ME RMSE MAE MPE MAPE MASE ACF1

## <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 arima_111_111 Test -0.000353 0.00823 0.00580 -0.0172 0.263 NaN 0.465

## 2 arima_202_210 Test -0.00348 0.00951 0.00732 -0.159 0.333 NaN 0.450

## 3 arima_400_011 Test -0.00904 0.0125 0.0108 -0.412 0.491 NaN 0.479

## 4 lm1 Test -0.00880 0.0121 0.0105 -0.401 0.477 NaN 0.471

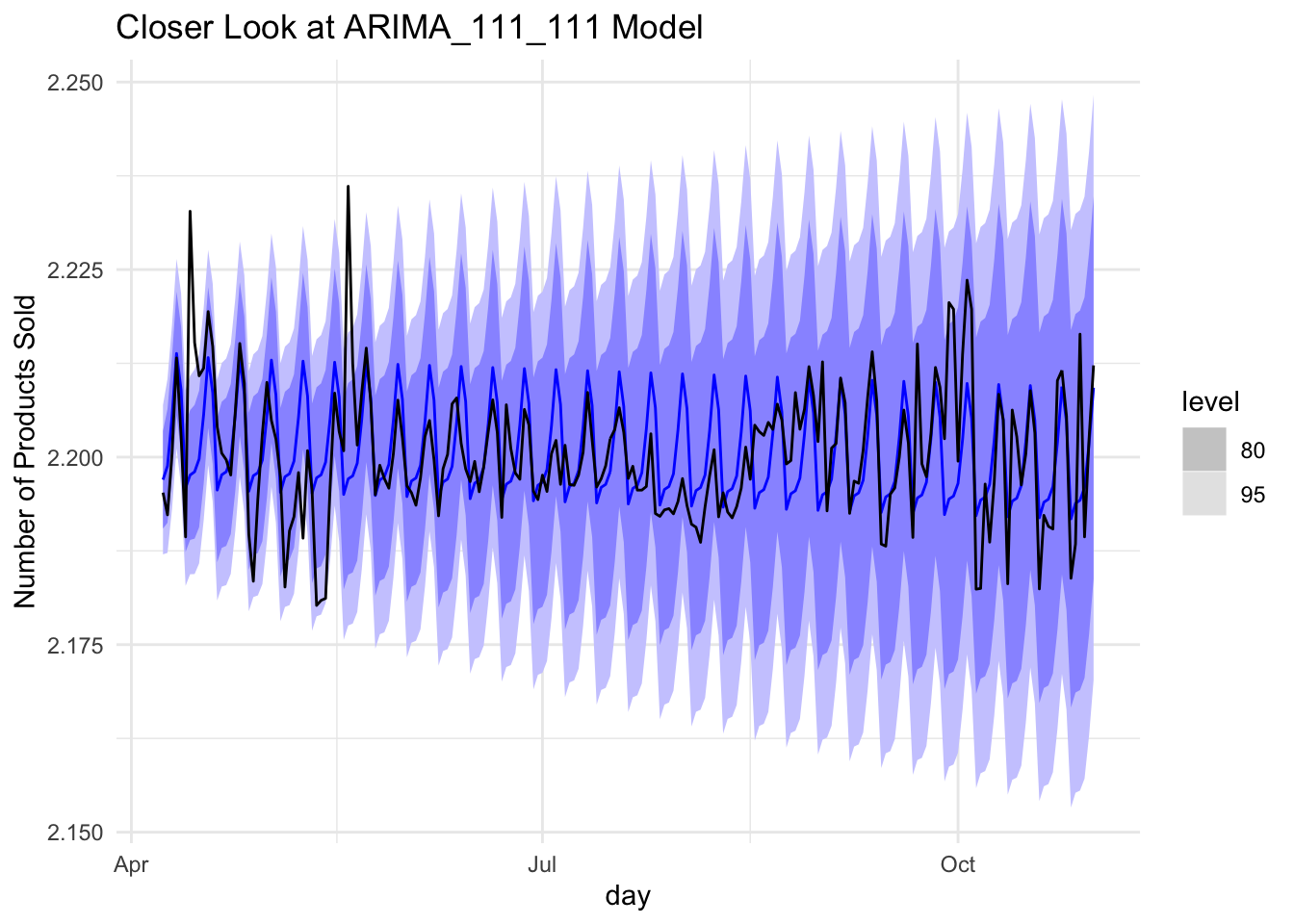

## 5 lm2 Test -0.00136 0.00900 0.00654 -0.0628 0.297 NaN 0.456A closer look at the arima_111_111 model on the test data

train %>%

model(ARIMA(item_cnt_day~pdq(1,1,1)+PDQ(1,1,1))) %>%

forecast(test) %>%

autoplot(test) +

xlab("day") +

ylab("Number of Products Sold") +

ggtitle("Closer Look at ARIMA_111_111 Model")

train %>%

model(ARIMA(item_cnt_day~pdq(1,1,1)+PDQ(1,1,1))) %>%

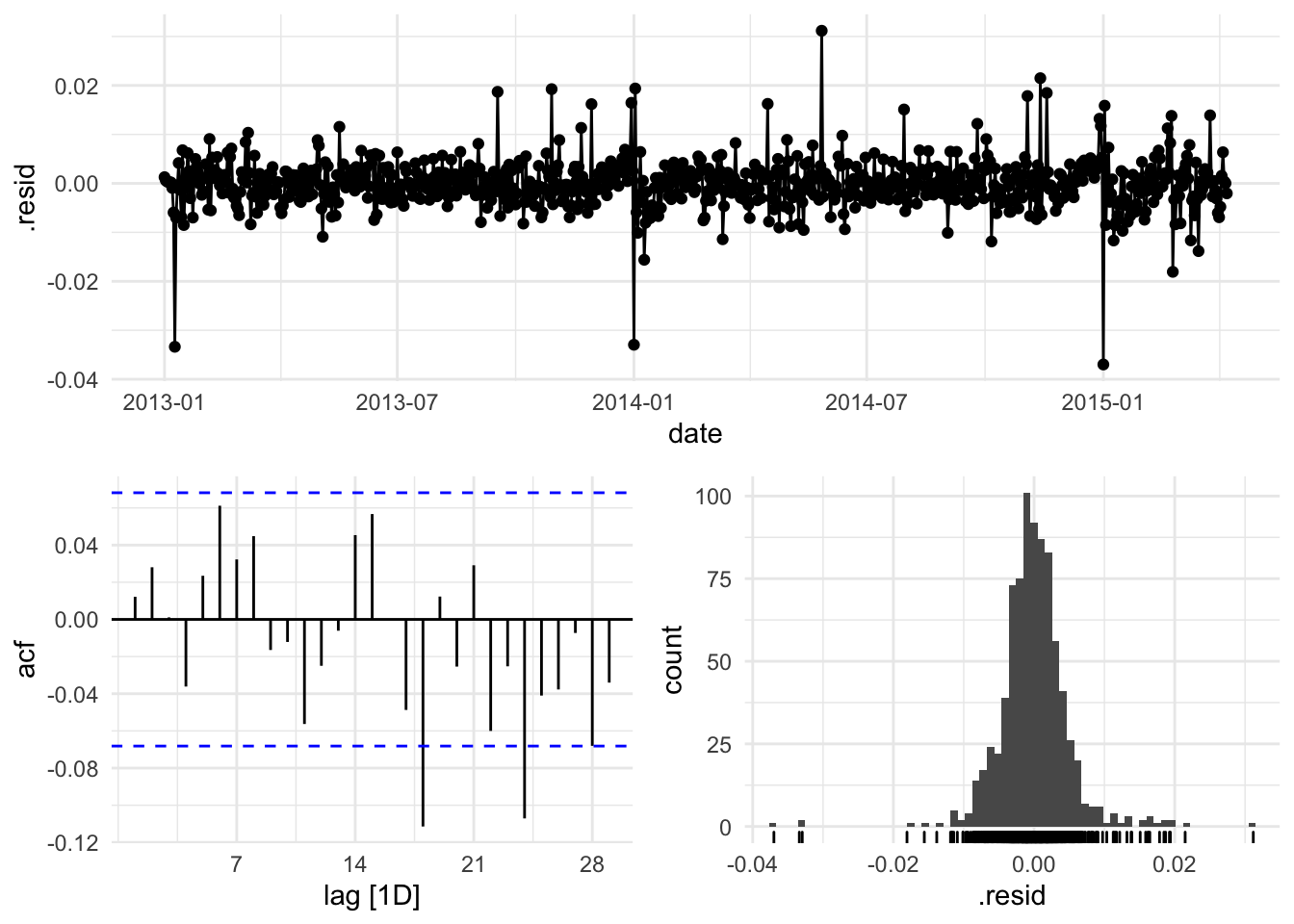

gg_tsresiduals()